Walk past any jeweller's row in Pettah, Maradana, or down Galle Road and the chalkboards tell the same story. The price per pawan keeps climbing — faster than most analysts expected at the start of 2026. The drivers aren't unique to Sri Lanka, but the way they land here certainly is.

The global picture

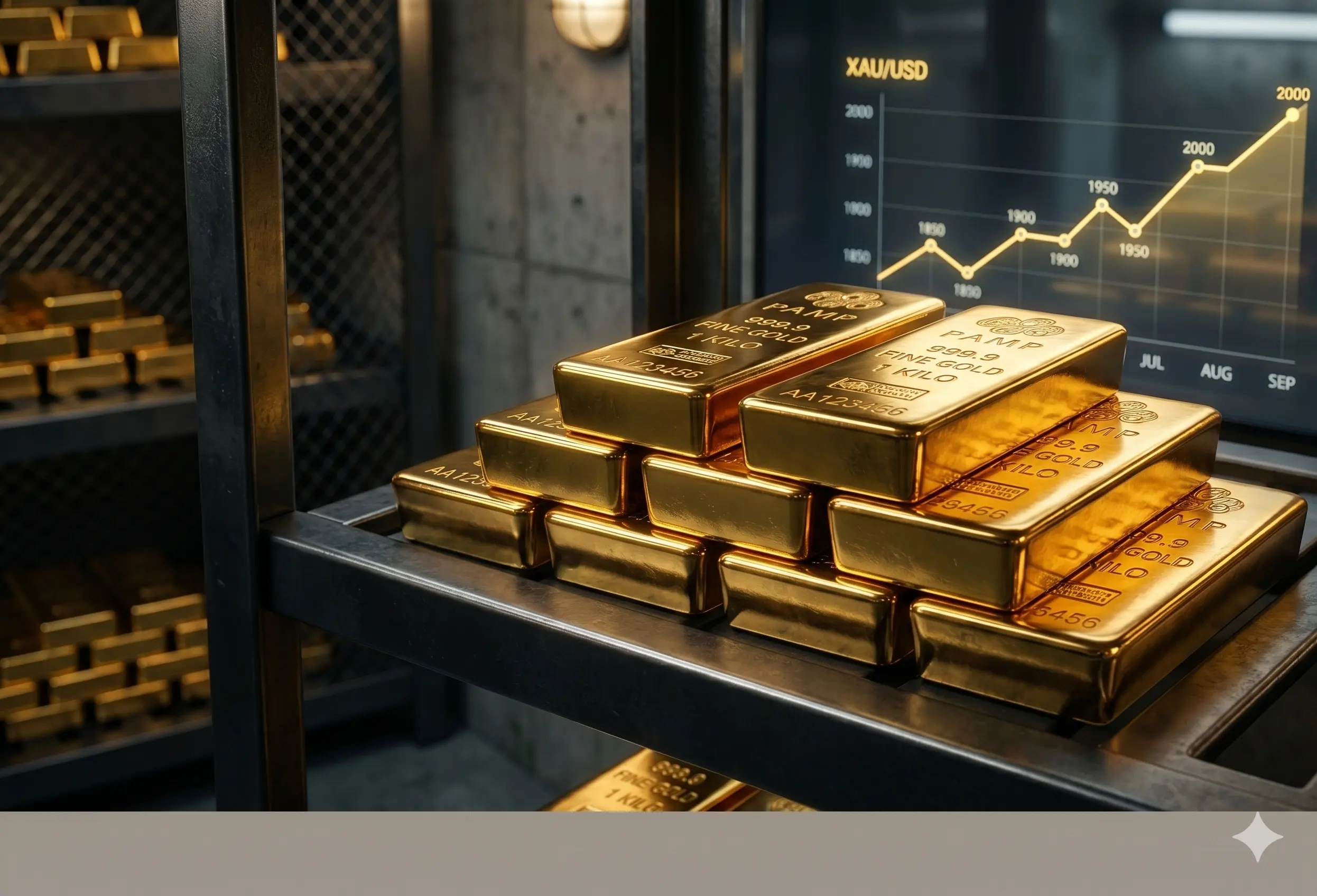

Three forces are pushing gold higher worldwide. First, the US Federal Reserve has begun a long-signalled rate-cutting cycle — and lower real yields almost always lift gold. Second, central banks in China, India, Türkiye and Poland have been buying bullion at the fastest pace in five decades, diversifying away from US treasuries. Third, geopolitical anxiety hasn't subsided, and gold remains the world's oldest safe-haven asset.

Add a softer US dollar to the mix and you have a near-perfect setup for a multi-year gold rally. International spot prices crossed historic milestones earlier this year and the move has been steadier than the spikes we saw in 2020 or 2008 which usually means the trend has more room to run.

What's amplifying it locally

Sri Lanka imports almost all of its gold. That makes the local per-pawan rate a product of two numbers: the international USD price, and the LKR–USD exchange rate. When both move in the same direction as they have for much of 2026 the local rate climbs faster than the global headline suggests.

- Rupee softness against the dollar, even after the post-IMF stabilisation, adds 3–5% on top of every global price move.

- Festive and wedding demand stays unusually firm families see gold as both ornament and insurance.

- Import duties and the bank-margin structure mean retail and pawn rates respond quickly to upward moves but slowly to downward ones.

- Informal pawn credit demand has risen with the cost of living, tightening physical gold supply on the open market.

What this means for sellers

If you've held gold for five years or more, you're now sitting on a meaningful gain often 60–90% in rupee terms, depending on purity and when you bought. For families considering an outright sale to fund a home renovation, an education, or a business, this is one of the better windows we've seen in a decade.

Our advice is always the same: get a transparent live-rate valuation in writing before committing to anything. The difference between a fair offer and a poor one can run into hundreds of thousands of rupees on a single wedding set.

What this means for pledge holders

This is the group that surprises people the most. If you pledged gold two or three years ago, the metal itself is now worth substantially more than the loan you took against it. Even after compounded interest and renewal fees, many of our clients find that settling the pledge today still leaves them with cash in hand — and their gold back.

“Every month you delay a settlement, the interest meter runs. But the price rise we're seeing right now is, for once, working in the pledge holder's favour.”

Where prices may go from here

No one calls the top on a gold rally with any reliability. What we can say is that the structural drivers — central bank buying, currency diversification, and persistent geopolitical risk — don't look likely to reverse in the next six to twelve months. Short-term pullbacks of 5–8% are normal in any uptrend, and they tend to be the moments where the smartest buyers step in.

If you're weighing a decision — to sell, to pledge, to settle, or to buy — talk to someone who works with live rates every day. We're always happy to walk you through the math without obligation.

Written by

Ran Naya Editorial Desk